Vietnam’s climate tech sector closed 2024 with its most significant funding milestone to date: more than $98 million raised across 55 deals. On the surface, it reads like a breakthrough year. A closer look reveals a more complex story of rapid growth, evolving capital, emerging sector leaders, and the founders building through persistent structural challenges.

These findings come from the Vietnam Climate Tech Funding Ecosystem 2025 report, jointly produced by New Energy Nexus Vietnam, RMIT University, and members of the AGILE Project (WUSC, Sarona Asset Management Fund).

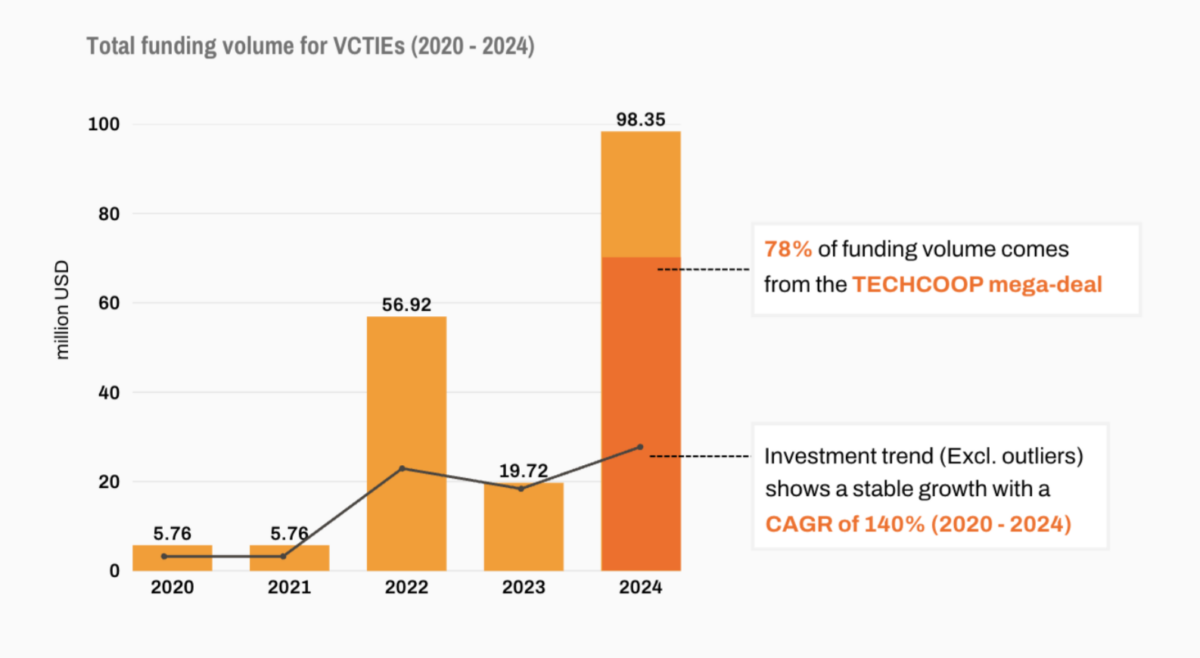

2024 – A historic funding year

The headline number is real, but context matters. Nearly 78 percent of 2024’s total funding volume came from a single transaction by TECHCOOP, a rising agricultural tech startup from Ho Chi Minh City. Even setting that megadeal aside, the underlying market tells an optimistic story: steady, disciplined investment growth at a compound annual growth rate of 140 percent since 2020. Climate tech is not just hype; it is a sector quietly building real foundations. Thirty-seven enterprises received funding, supported by 31 active funders — numbers that suggest less a speculative rush than a community of believers making deliberate bets on Vietnam’s green future.

Energy Transition is pulling away from the pack

After removing the megadeal effect from 2024, energy transition emerges as the fastest-growing climate tech segment, with funding increasing fivefold to $15.5 million across 15 deals, driven by solar energy, energy storage, and efficiency solutions.

The alignment with Vietnam’s national energy roadmap, PDP VIII, is not coincidental: policy tailwinds are creating real commercial opportunity. Other segments, meanwhile, recorded stagnant growth — the built environment (sustainable HVAC, smart grid, and related solutions) saw no new deals in 2024.

The funding mix is changing rapidly

Vietnam’s climate tech financing is no longer synonymous with venture capital. Non-equity instruments—debt, convertible notes, grants, and prize money—jumped from just 4.3 percent of funding volume in 2022 to more than 41 percent in 2024. These financing models primarily serve climate tech SMEs in the “missing middle”: firms too small for private equity, too large for microfinance, outside the hyper-growth profile venture capital requires, and unable to access bank loans due to collateral or eligibility constraints.

Impact capital has arrived, and it expects results

Perhaps the most consequential structural shift is the rise of impact investors, whose participation grew tenfold between 2020 and 2024. These are not passive funders. They expect measurable decarbonization data, social inclusion metrics, milestone-based disbursements, and governance systems that meet IFC and DFI standards. For founders, the era of storytelling alone is over. The new currency is integrated evidence: impact and bankability presented as a single, coherent case backed by real operational data. Founders who build that capability early will have a meaningful competitive edge.

Though women are driving climate tech, they are still facing unnecessary headwinds

One of the most striking findings in the report: 47.2 percent of funded climate tech enterprises in Vietnam in 2024 were co-founded by women. That significantly outpaces global averages, where female founder representation in climate tech has only recently climbed to 21.7 percent. Yet structural barriers persist — household time burdens, “boys’ club” investor networks, and the limited prioritization of DEI within climate tech companies continue to constrain what women can achieve in the ecosystem. Many enterprises still lack formal DEI or non-discrimination policies; as one founder noted, “I say there is no such policy simply because we don’t practice any discrimination.” The women themselves are clear: they do not want to be funded because of their gender. They want to be judged on technology, team, and fundamentals. The ecosystem’s job is to make sure those fundamentals are what actually determine outcomes.

Organizers and Participants of Deltaccelerate, an accelerator program dedicating towards women-led enterprises adapt to climate change

These five findings are just the surface. Behind each one sits a deeper body of data, expert perspectives, founder interviews, and actionable recommendations for every stakeholder in the ecosystem—from early-stage startups to institutional funders and policymakers.

The research team is also launching a survey for report readers to gather valuable feedback for the 2026 edition.